Understand the importance of capital investment planning and appraisal. Learn about the key investment appraisal techniques. Understand the importance of human behaviour issues in investment decision making.

Need For Investment Appraisal?

Businesses need to make investments and the nature of investment decisions is such that large amounts of resources are often involved and relatively long timescales are involved. It is also often difficult or expensive to bale out of an investment once it is undertaken.

Capital investment appraisal methods are techniques used by businesses and investors to evaluate potential investments and determine whether they are profitable or not. The purpose of capital investment appraisal is to provide decision-makers with a way to compare the costs and benefits of different investment options.

Some common Capital investment appraisal methods include Payback, Discounted Payback, Accounting Rate of Return (ARR). Net Present Value (NPV), Internal Rate of Return (IRR)

Each of these methods has its own strengths and weaknesses, and businesses must choose the method that best suits their needs and goals.

Here’s how investment decisions are managing in most firms.

- Determine investment funds available

- Identify profitable project opportunities

- Refine and classify proposed projects

- Evaluate the proposed project(s)

- Approve the project(s)

- Monitor and control the project(s)

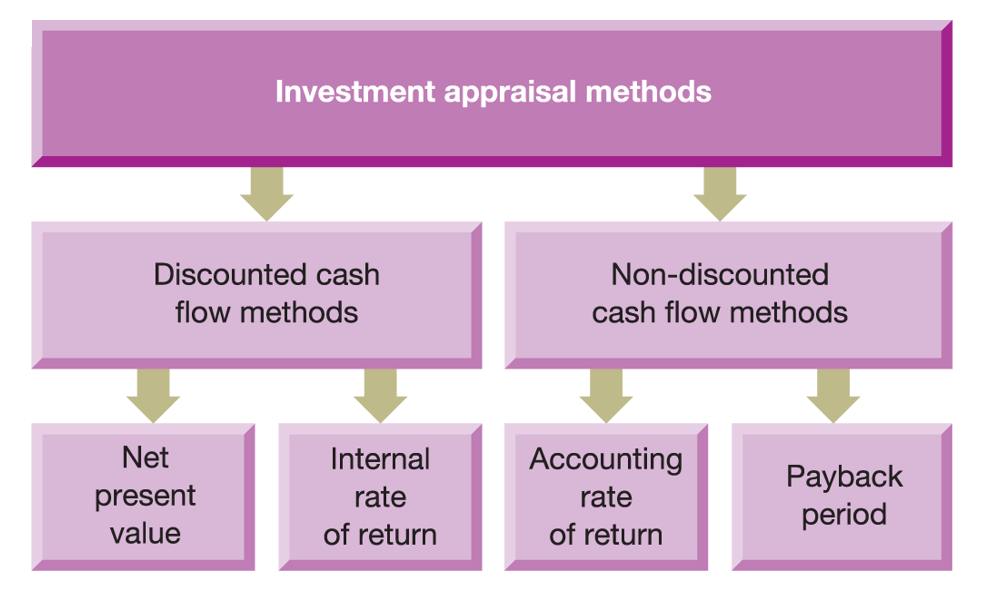

Non-DCF Investment Appraisal Methods

Accounting Rate of Return (ARR)

ARR = (Average annual operating profit) / (Average investment to earn that profit) x 100%.

ARR decision rule

For a project to be acceptable, it must achieve at least a minimum target ARR. Where competing projects exceed the minimum rate, the one with the highest ARR should be selected.

Limitations of ARR

- Ignores the timing of cash flows

- Use of average investment

- Use of accounting profit

- Competing investments

Payback period

Time taken for initial investment to be repaid out of project net cash inflows.

Many firms use the pay-back period as an accept or reject criterion as well as a method of ranking projects.

If the pay-back period calculated for a project is less than the maximum pay-back period set by management, it would be accepted; if not, it would be rejected. As a ranking method, it gives highest ranking to the project which has shortest pay-back period and lowest ranking to the project with highest pay-back period.

Thus, if the firm has to choose among two mutually exclusive projects, project with shorter pay-back period is selected.

Payback period decision rule:

Project should have a shorter payback period than the required maximum payback period. If competing projects have payback periods shorter than maximum payback period, the one with the shortest payback period is selected.

Advantage of pay-back method is that it is easy to calculate and simple to understand.

Limitations of Payback period:

- It does not take into account the cash inflows earned after the pay-back period and hence the true profitability of the project cannot be correctly assessed.

- It ignores time value of money. Cash flows received in different years are treated equally.

- It does not take into consideration the cost of capital which is a very important factor in making a sound investment decisions.

- Arbitrarily determined target payback period

DCF Investment Appraisal Methods

DCF stands for Discounted cash flow. This method considers all of the cash flows for each investment opportunity.

Net Present Value (NPV) and Internal Rate of Return (IRR) are the more commonly used DCF investment appraisal methods. These make a logical allowance for the timing of those cash flows.

DCF method (NPV/IRR) is better than Non-DCF method (ARR and PP) due to the following reasons:

- It considers timing of the cash flows, and the whole of the relevant cash flows

- It considers the objectives of the business

Net Present Value (NPV) Method

Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present.

In this method present values of cash outflow & inflows are calculated; for calculating this, a discounting factor is consider i.e. cost of capital.

NPV = Discounted cash inflows – discounted cash outflows.

NPV decision making (Acceptance or reject criterion):

The NPV can be used as an “accept or reject” criterion in case NPV is positive, the project should be accepted however is NPV in negative, the project should be rejected.

NPV = (Cash Flow / (1 + i) raised to t) – Initial Investment

i = Required return or discount rate

t = Number of time periods

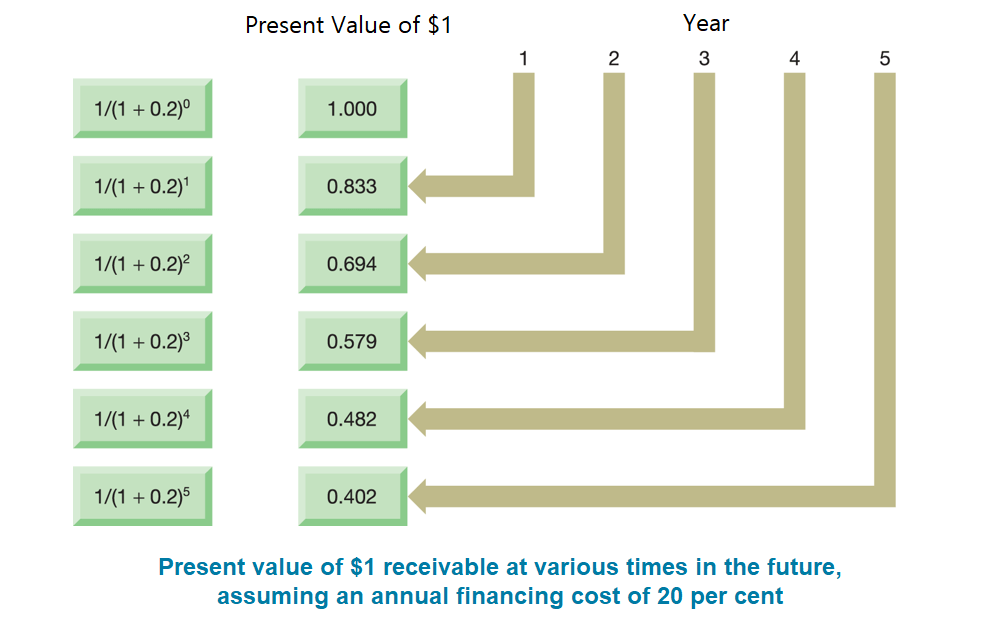

The present value of a cash flow:

PV of the cash flow of year n = actual cash flow of year n divided by (1 + r)n

Cut off point: The cut-off point refers to the point below which a project would not be accepted. For Example, if 10% is the desired rate of return, the cut-off rate is 10%. The cut-off point may also be in terms of period. For example, if the management desires that the investment in the project should be recouped in three years, the period of three years would be taken as the cut-off period. A project, incapable of generating necessary cash to pay for the initial investment in the project within three years, will not be accepted.

Merits of Net Present Value Method:

The merits of this method of evaluating investment proposal are as follows:

- This method considers the entire economic life of the project.

- It takes into account the objective of maximum profitability.

- It recognizes the time value of money.

- This method can be applied where cash inflows are uneven.

- It facilitates comparison between projects.

NPV takes account of key factors (interest foregone, risk premium, inflation) influencing the return required by investors from a project.

Demerits of this method are as follows:

- It is not easy to determine an appropriate discount rate.

- It involves a great deal of calculations. It is more difficult to understand and operate.

- It is very difficult to forecast the economic life of any investment exactly.

- It may not give good results while comparing projects with unequal investment of funds.

Internal rate of return (IRR)

Internal rate of return (IRR) give a DCF value of $0.

IRR is the discount rate, which, when applied to the future project cash flows, produces a zero NPV.

IRR decision rule

Project must meet a minimum IRR requirement (The opportunity cost of finance). If competing projects exceed minimum IRR requirement, the one with the highest IRR is selected.

Limitations of IRR

- Does not directly address wealth maximisation.

- Ignores the scale of investment.

- Has difficulty with unconventional cash flows.

Investment Appraisal in Practice

Many surveys have shown the following features:

- Businesses tend to use more than one method

- NPV and IRR have become increasingly popular

- Continued popularity of the PP and ARR methods

- Larger businesses rely more heavily on NPV and IRR than smaller businesses

Where projects are divisible, managers should seek to maximise the present value per dollar of scarce resource

Profitability index (PI) allows ranking of projects based on NPV

PI = (PV of future cash flows) / (Initial outlay)

Inflation and investment appraisal

Two possible approaches (both methods, properly applied, will give the same result):

- Adjust future cash flows for inflation and use a discount rate that is also adjusted for inflation

- Exclude inflation from the future cash flows and use a ‘real’ discount rate that excludes inflation

Here are some more factors to consider.

Investment appraisal and risk

Risk is important because of the long timescales involved and the size of the investment made.

Scenario analysis is a technique that is commonly used to evaluate the potential performance of various investments under different scenarios.

Risk Factors that must be used in scenario analysis that affects the sensitivity of NPV calculations include Annual sales volume, Life of machine, Initial outlay, Operating costs, Financing cost, Sales price.

Behavioural Points

Behavioural aspects in investment decisions are the psychological and emotional factors, such as biases, emotions, and heuristics, that can influence an investor’s decision-making process.

These factors can lead investors to make suboptimal investment decisions, which can result in financial losses.

There are several behavioural aspects in investment decisions.

- Accounting data used is subjective and can be manipulated

- Management may also seek to “empire build”.

- Lack of post completion audit may allow false promises to be made on investment returns

- Managers may compete with each other to get their own investment projects approved rather than seek the best alternative for the company.

As such, it is important for managers to be aware of these behavioral aspects and to take them into account when making investment decisions.

Related: Finance and Accounting for Managers

Leave a Reply